Step 1

Weeks 1–2

Weeks 1–2

Initial Assessment & Corporate Structuring

What we do: We map your existing business against UKGC requirements and identify structural gaps before any application work begins. This prevents costly restructuring mid-process.

Licence type selection — we determine which operating licence categories you need: remote casino, betting, bingo, poker, or a combination, and whether a personal management licence is required immediately or can follow

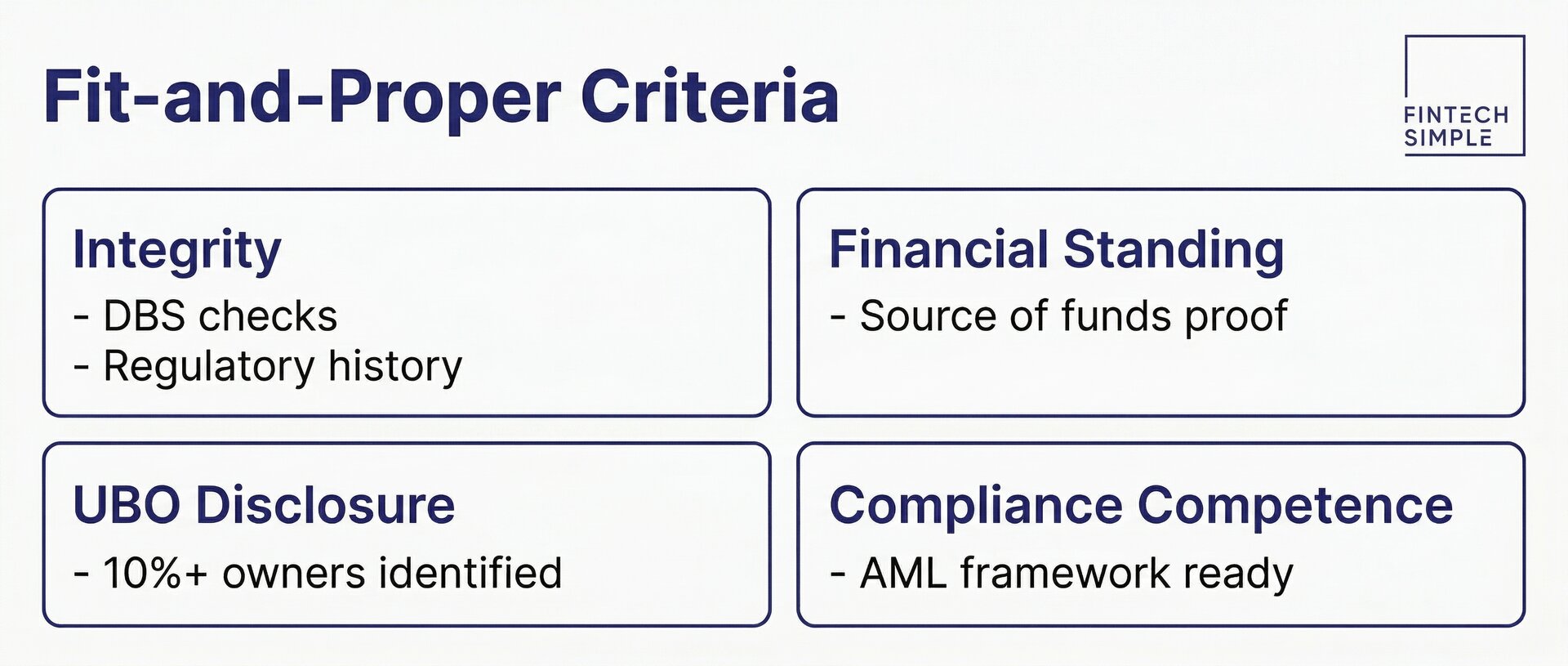

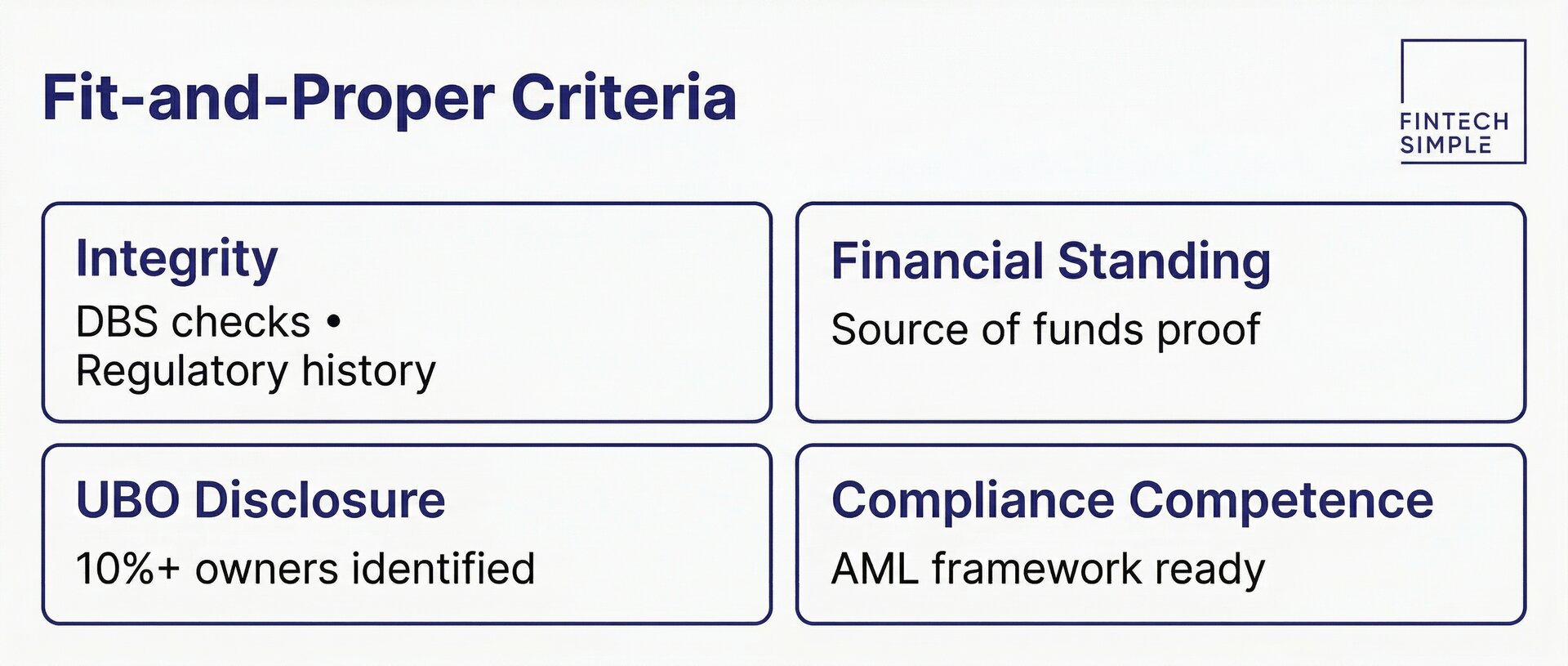

Licence type selection — we determine which operating licence categories you need: remote casino, betting, bingo, poker, or a combination, and whether a personal management licence is required immediately or can follow- Corporate structure review — we assess your holding company, shareholders, and UBO chain against UKGC fit-and-proper standards. Non-EEA structures often require additional disclosure layers

- Source of funds mapping — we document the provenance of capitalisation funds, which the UKGC checks against AML red flags from day one of review

- Gap analysis report — you receive a written list of missing documents, structural changes needed, and estimated costs before work proceeds