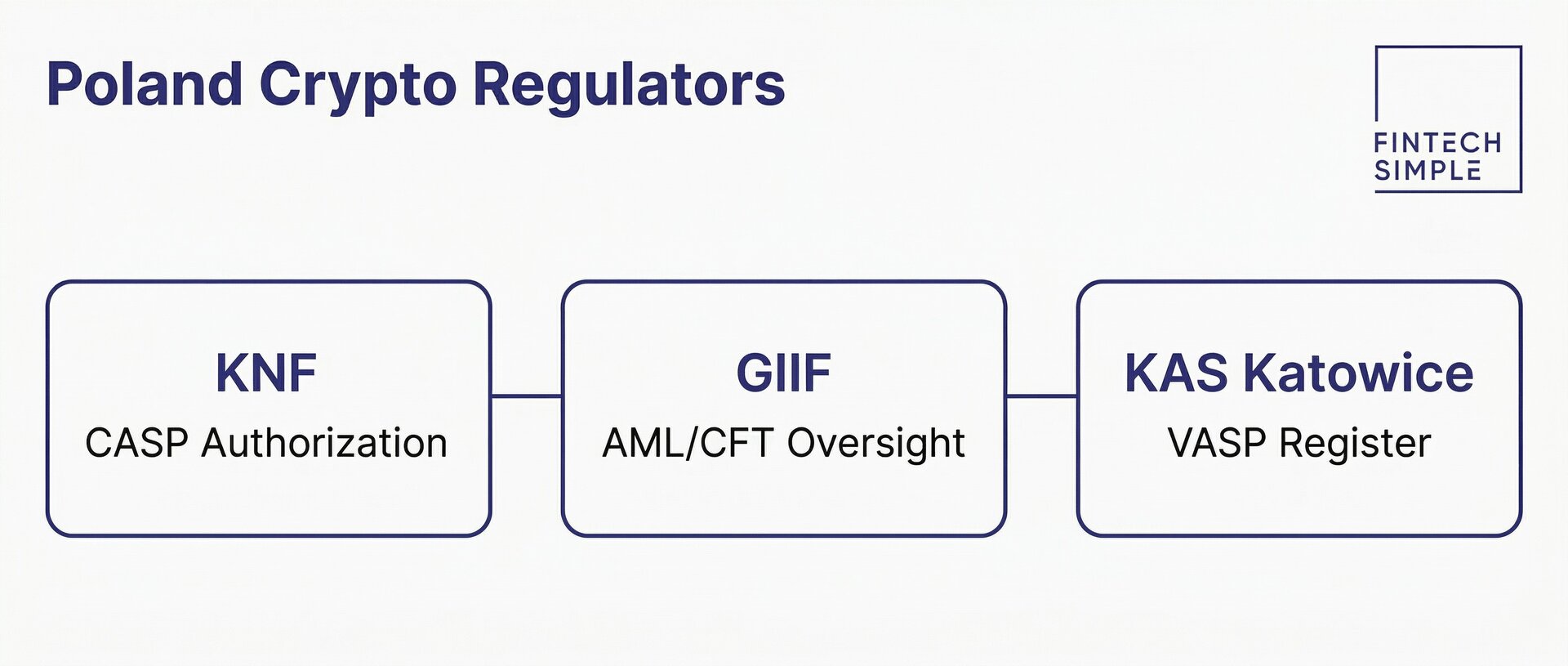

VASP violations cover failures under the domestic AML/CFT regime — for example, operating without registration, failing to perform customer due diligence, or not filing suspicious transaction reports with the General Inspector of Financial Information (GIIF). KNF may impose an administrative fine of up to 100,000 PLN per individual breach, and fines can accumulate across multiple simultaneous violations.

CASP violations under MiCA apply from the date MiCA became fully applicable. KNF, acting as the competent authority designated under MiCA Article 93, can impose fines of up to €5,000,000 on legal persons, or up to 10% of total annual turnover — whichever figure is higher. For natural persons, the ceiling is €700,000. Aggravating factors include repeat offences, intentional conduct, and harm caused to clients.

AML criminal liability targets the most serious breaches — deliberately facilitating money laundering or terrorist financing through a crypto business. Conviction carries a custodial sentence ranging from 3 months to 5 years. Prosecutors can pursue individuals at the director or beneficial-owner level, not just the entity.

KNF enforcement powers extend beyond fines. The regulator can suspend a CASP’s authorisation, prohibit it from onboarding new clients, require it to cease specific activities, or revoke the licence entirely. KNF also publishes enforcement decisions on its website, creating significant reputational exposure alongside the financial penalty. Any business operating in Poland — or passporting into Poland under MiCA — should treat KNF’s supervisory capacity as a live operational risk.

Week 1

Week 1

Activity scoping — exchange, custody, transfer, or a combination; each carries distinct compliance requirements

Activity scoping — exchange, custody, transfer, or a combination; each carries distinct compliance requirements