Step 1

Weeks 1–2

Weeks 1–2

Pre-engagement and scoping

What we do: We map your target activity mix (Cat. 1 e-money issuance, Cat. 2 payment services, MiCA EMT overlay) against MFSA expectations, then size capital, governance and the realistic timeline before any cost is committed.

-

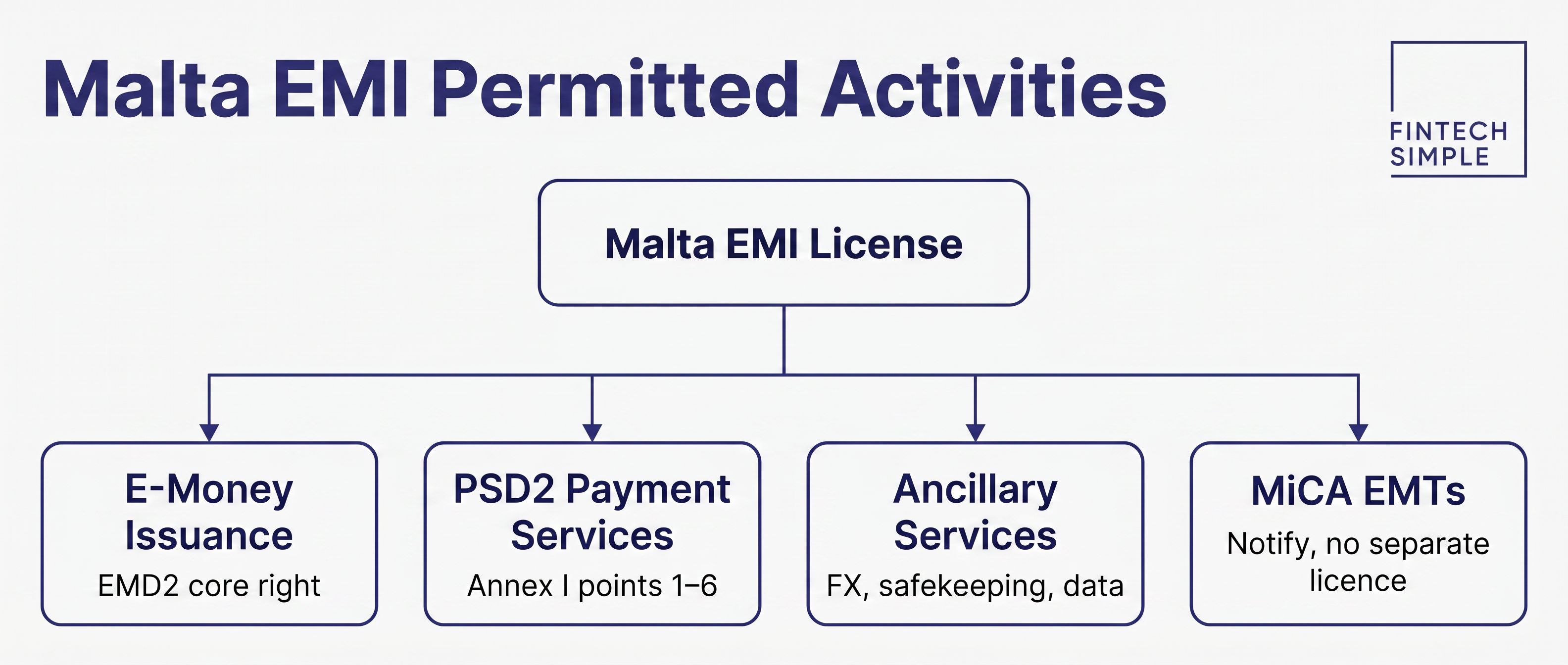

Activity-scope analysis: e-money issuance plus the specific PSD2 Annex I services you need, with MiCA EMT layered in where stablecoins are part of the model

Activity-scope analysis: e-money issuance plus the specific PSD2 Annex I services you need, with MiCA EMT layered in where stablecoins are part of the model

-

Capital and own-funds modelling: €350,000 initial baseline plus the FIR/03 ongoing calculation against projected outstanding e-money

-

Engagement letter and Year-1 budget: advisory fees, MFSA fees, capital, premises, staffing and audit set out in a single forecast