Step 1

Weeks 1–3

Weeks 1–3

Initial Assessment & Entity Setup

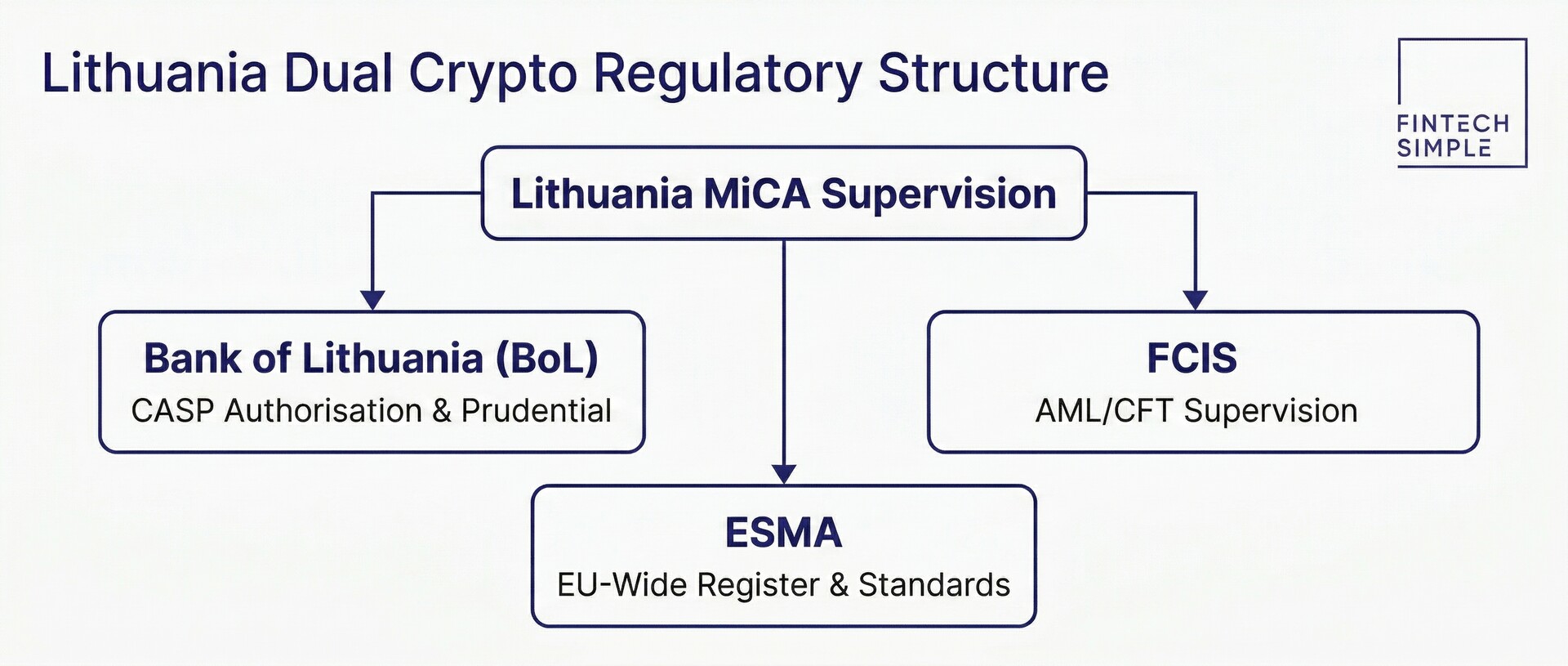

What we do: We map your business model against the ten crypto-asset service categories defined in MiCA Article 3(1)(16) (custody & administration, operation of a trading platform, exchange against fiat, exchange crypto-to-crypto, execution of orders, placement, reception & transmission of orders, advice, portfolio management, and transfer services) and identify exactly which authorizations you need. We then incorporate a Lithuanian private limited company (UAB) or, if you already have one, verify it meets Bank of Lithuania structural requirements.

CASP class selection — determine the precise combination of services to avoid over-licensing (higher capital) or under-licensing (enforcement risk).

CASP class selection — determine the precise combination of services to avoid over-licensing (higher capital) or under-licensing (enforcement risk).- Legal entity — register a UAB with a physical registered office in Lithuania; a virtual address does not satisfy the regulator.

- Share structure & UBO mapping — document ultimate beneficial owners holding ≥10% and prepare the ownership chart required in the application.

- Grandfathering check — if you held a pre-MiCA Lithuanian VASP registration, we confirm eligibility for the conversion pathway and note which documents can be reused.

- Initial capital confirmation — verify you meet the relevant MiCA minimum (€50,000 for Class 1 CASPs, €125,000 for Class 2 including custody and exchange services, €150,000 for Class 3 trading-platform operators) before the application clock starts.