Labuan has real advantages, but it also has real drawbacks. Before committing capital and management time to this jurisdiction, you should understand what consistently causes problems for licensees. These are not edge cases; they affect most applicants at some point.

Banking is the biggest practical obstacle. Opening a corporate bank account for a Labuan crypto entity takes longer and fails more often than in comparable jurisdictions. Most Malaysian banks either refuse crypto businesses outright or impose months-long due diligence processes with no guaranteed outcome. Many licensees end up relying on EMIs or payment processors in third countries, which adds cost and complexity. Fintech Simple manages introductions to account-friendly institutions, but we will not oversell this: banking for crypto remains harder in Labuan than in the UAE or Lithuania.

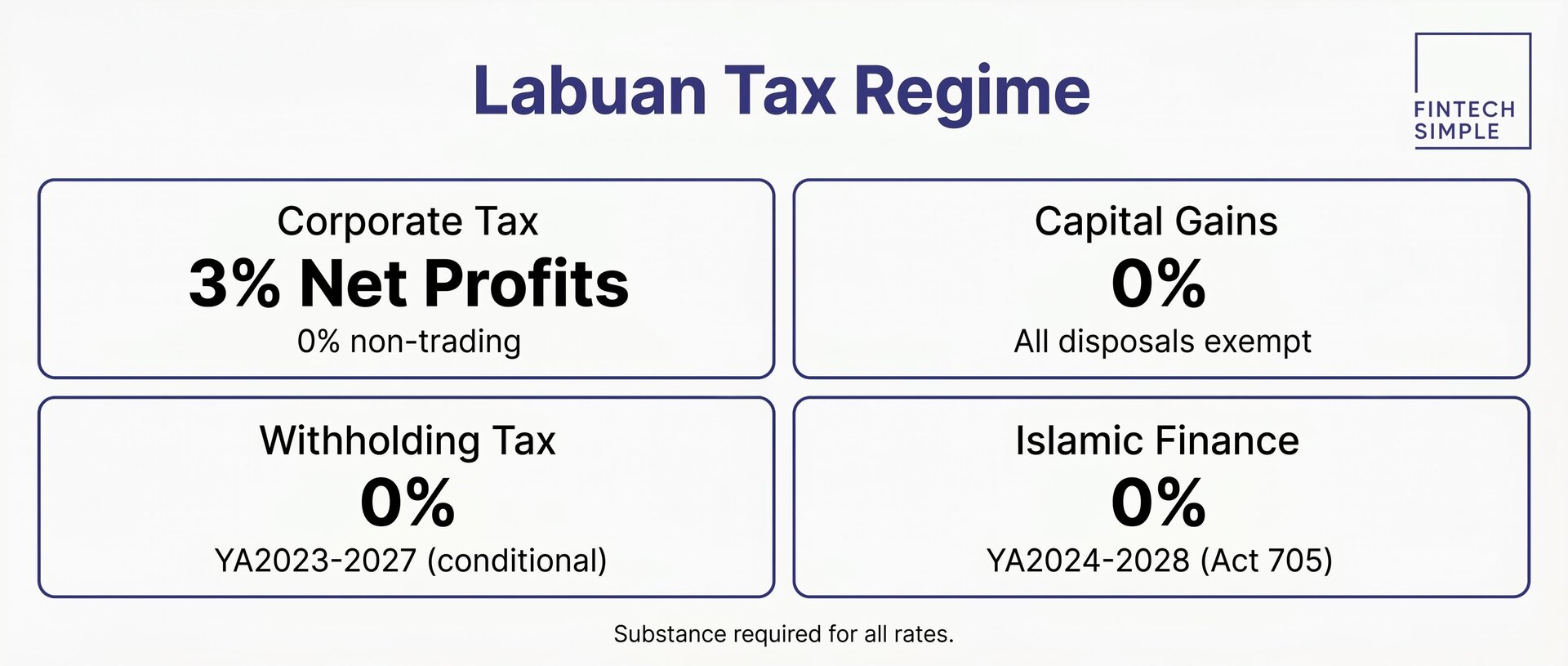

Economic substance is a real operational burden, not a checkbox. The substance requirements are enforced through annual reporting with no grace period. Failure triggers the standard Malaysian corporate tax rate of 24% instead of the preferential 3%.

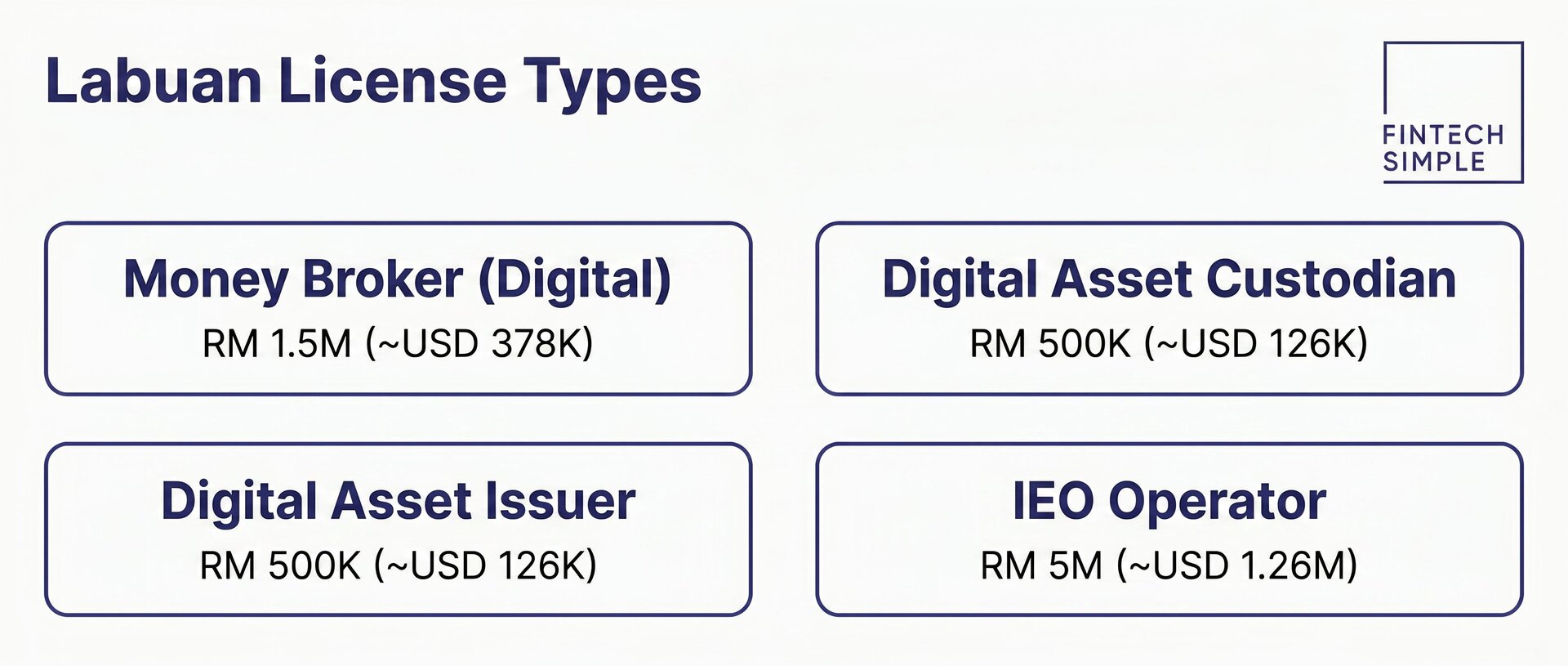

Regulatory fees are rising sharply. LFSA revised its fee structure effective 1 January 2026. The annual licence fee for a Money Broker (Digital Asset) license is USD 10,000 from 2026 for new licensees. Existing licensees benefit from a transitional schedule: USD 1,500 in 2026, USD 5,750 in 2027, and USD 10,000 from 2028. A separate one-time application fee of USD 500 also applies. Ongoing cost projections must account for these scheduled increases.

Competition from UAE and Singapore has intensified. Both jurisdictions now offer stronger international banking access and more globally recognised regulatory brands for crypto businesses targeting institutional clients. Labuan competes primarily on cost and speed for operators who do not need MAS or VARA-level recognition. See the full comparison for a detailed breakdown.

Political and regulatory uncertainty is a long-term consideration. Malaysia’s policy environment for crypto is still maturing. LFSA has updated its guidelines, fee schedules, and substance requirements multiple times since 2021. The current preferential tax treatment, including specific income exemptions between Labuan entities under P.U.(A) 59/2025 covering YA 2023–2027, is conditional and time-limited. Operators building a long-term structure should model scenarios in which the tax and fee landscape continues to tighten.

Weeks 1–3

Weeks 1–3

Directors — appoint at least 2 directors (natural persons), including at least one resident director; each must evidence 3–5 years of relevant financial services experience

Directors — appoint at least 2 directors (natural persons), including at least one resident director; each must evidence 3–5 years of relevant financial services experience